2026 Mid-Year Life Sciences Real Estate Outlook: How Today's Market Is Reshaping Lab Space Strategy

After a decade of unprecedented expansion in the 2010s, followed by post-pandemic upheaval, financial pullback, and market oversupply challenges, the Bay Area life sciences real estate market is entering a period of normalization. Occupancy has recovered from the elevated vacancy rates seen in the early 2020s, while remaining below the historically high occupancy levels that characterized the market's peak. The result is a more balanced environment that provides greater flexibility for occupiers without diminishing the long-term strength of the region's life sciences ecosystem.

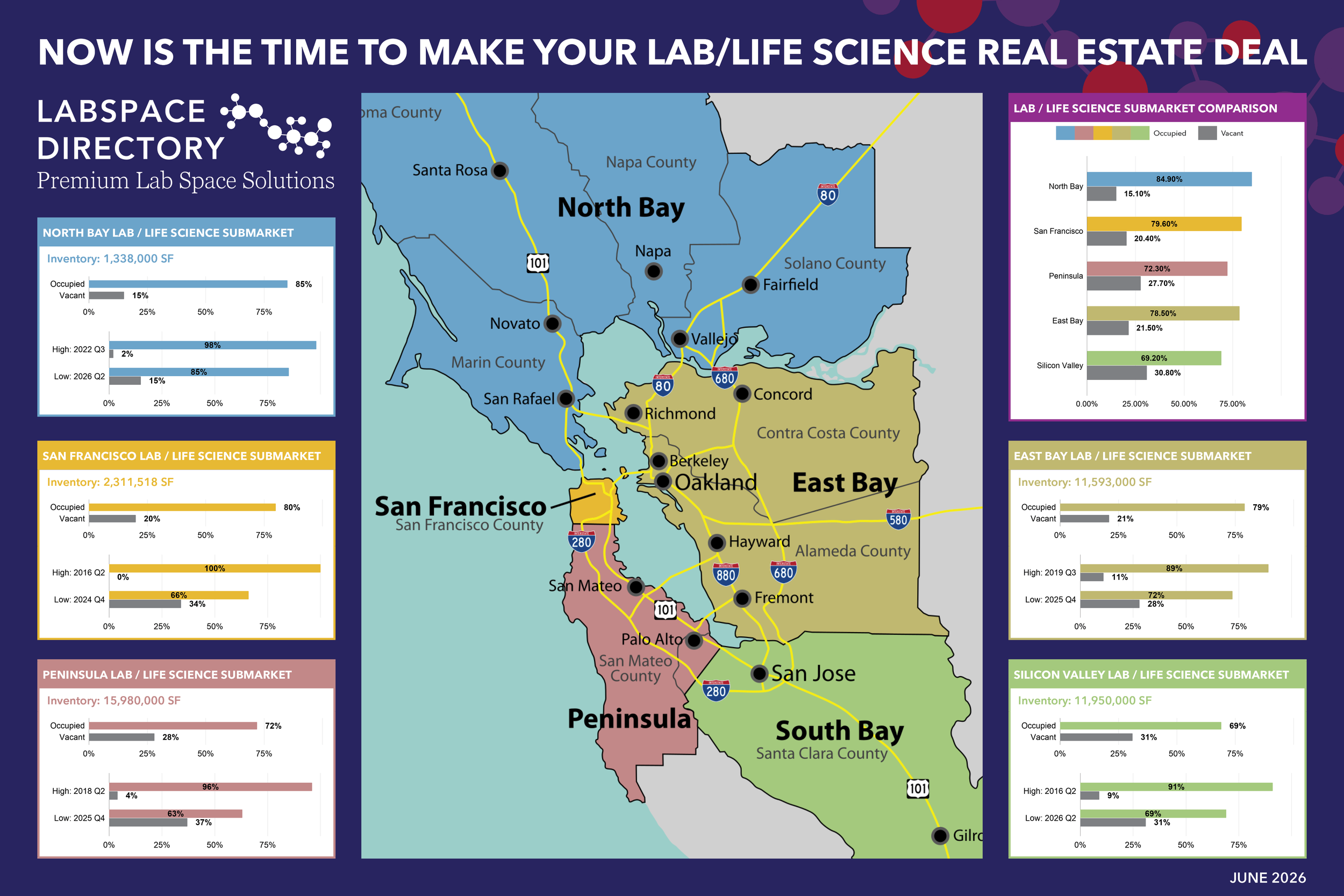

According to Labspace Directory's Bay Area market data, occupancy levels now range from 69.2% in Silicon Valley to 84.9% in the North Bay, creating substantially more options for occupiers than were available during the market's peak expansion years.

The change becomes even more apparent when compared to historical highs. Silicon Valley occupancy has declined from 91% in 2016 to 69% in 2026, while the Peninsula has fallen from 96% occupancy in 2018 to 72% today. Similar trends are visible across the East Bay, San Francisco, and North Bay submarkets. In line, construction pipelines have slackened, logistic constraints have eased, for now, slowing cost increases and reducing delivery delays.

For founders and growing biotech companies, these conditions have created a rare opportunity to negotiate more favorable lease terms, secure higher-quality equipment and facilities at lower cost, and evaluate multiple locations before making a commitment.

"The Bay Area remains one of the most strategically important life sciences markets in the world. What has changed is that tenants now have more leverage and more choices than they've had in years. Companies that plan ahead can secure the right lab space to position themselves for long-term growth while taking advantage of today's tenant-favorable market conditions,” said David Klein, Esq. CCIM SIOR LEED AP MCR, Co-Founder of Labspace Directory.

The Bay Area Remains a Global Life Sciences Powerhouse

The San Francisco Bay Area remains one of the largest and most established life sciences ecosystems in the world. Labspace Directory currently tracks more than 43 million square feet of life sciences inventory across the region's primary submarkets, making it one of the country's most active and diverse life sciences real estate markets.

Bay Area Life Sciences Inventory by Submarket

Peninsula: 15.98M SF

Silicon Valley: 11.95M SF

East Bay: 11.59M SF

San Francisco: 2.31M SF

North Bay: 1.34M SF

The Peninsula continues to serve as the region's largest life sciences cluster, benefiting from its proximity to South San Francisco – the nucleus of the Bay Area’s life science community, venture capital firms, leading research institutions, and a deep talent pool. However, increasing availability across the region is giving occupiers greater flexibility when evaluating their location strategy.

How Space Strategy Is Changing in 2026

As market conditions evolve, life science companies are rethinking how they approach real estate decisions. During the peak of the market, many occupiers focused primarily on securing available space before competitors could act with cost a secondary consideration.

Today, the conversation has shifted from availability to optimization. For laboratory owners and developers, this shift means understanding what tenants value most. Rather than leasing for immediate needs alone, founders are taking a more strategic view of occupancy costs, future headcount growth, infrastructure requirements, and long-term flexibility. Companies now have greater opportunities to negotiate lease concessions, secure expansion rights, and evaluate multiple submarkets before making a commitment.

"The companies that will benefit most from today's environment aren't necessarily the ones chasing the lowest occupancy cost," said Elijah (E.J.) Hodges, Co-Founder of Labspace Directory. "They're the organizations aligning real estate decisions with talent access, infrastructure requirements, funding timelines, and long-term growth objectives."

The result is a more disciplined market for both occupiers and owners. Occupiers have become more selective, while owners are increasingly focused on differentiating their properties through access, quality, flexibility, and life science-specific amenities.

Unlike traditional commercial real estate, life sciences facilities are purpose-built environments that must accommodate specialized infrastructure, including robust utilities, ventilation systems, hazardous material storage and disposal, cleanrooms, and highly customized laboratory layouts. Whether a company operates a wet lab, dry lab, or biomanufacturing facility, the lab space must support its unique scientific, operational, and regulatory requirements.

A Market Reset, Not a Market Retreat

Some observers interpret rising or continued vacancy as a sign of weakening demand. A more accurate assessment is that the market is experiencing a recalibration after an extraordinary growth cycle.

Across multiple Bay Area submarkets, occupancy remains well above levels that would suggest long-term structural weakness in the Bay Area life sciences market. Even Silicon Valley, currently the region's softest major market at 69.2% occupancy, still maintains nearly 12 million square feet of active life sciences inventory. However, the AI effect has only just begun to affect life science work and space demand, with the elimination of some job positions in assaying and other repeatable lab processes. The net result on real estate is yet to be isolated and measured.

For founders, this means greater negotiating leverage. For owners, it means differentiating through infrastructure, amenities, and flexibility. For both groups, it reinforces the importance of making decisions based on localized market intelligence rather than national headlines.

Looking Ahead

While the life sciences real estate market has undeniably shifted since its peak expansion years, the underlying drivers of demand remain strong. Breakthrough research, continued investment in biotechnology, and the ongoing need for laboratory and innovation space continue to support long-term growth across major life sciences markets.

For founders evaluating their next lab space or life sciences facility and owners positioning assets for future demand, 2026 presents a unique opportunity to make strategic decisions from a position of greater market visibility and flexibility. Organizations that take advantage of current conditions while planning for future growth will be best positioned to succeed as the market enters its next phase.

As the life sciences real estate market continues to evolve, access to timely, localized market intelligence will remain essential for founders, occupiers, investors, and property owners making long-term real estate decisions. Whether you're evaluating your first lab space, planning an expansion, or tracking Bay Area life science market trends, Labspace Directory provides current market data, available lab space listings, and industry insights to support organizations make informed decisions.